market volatility

-

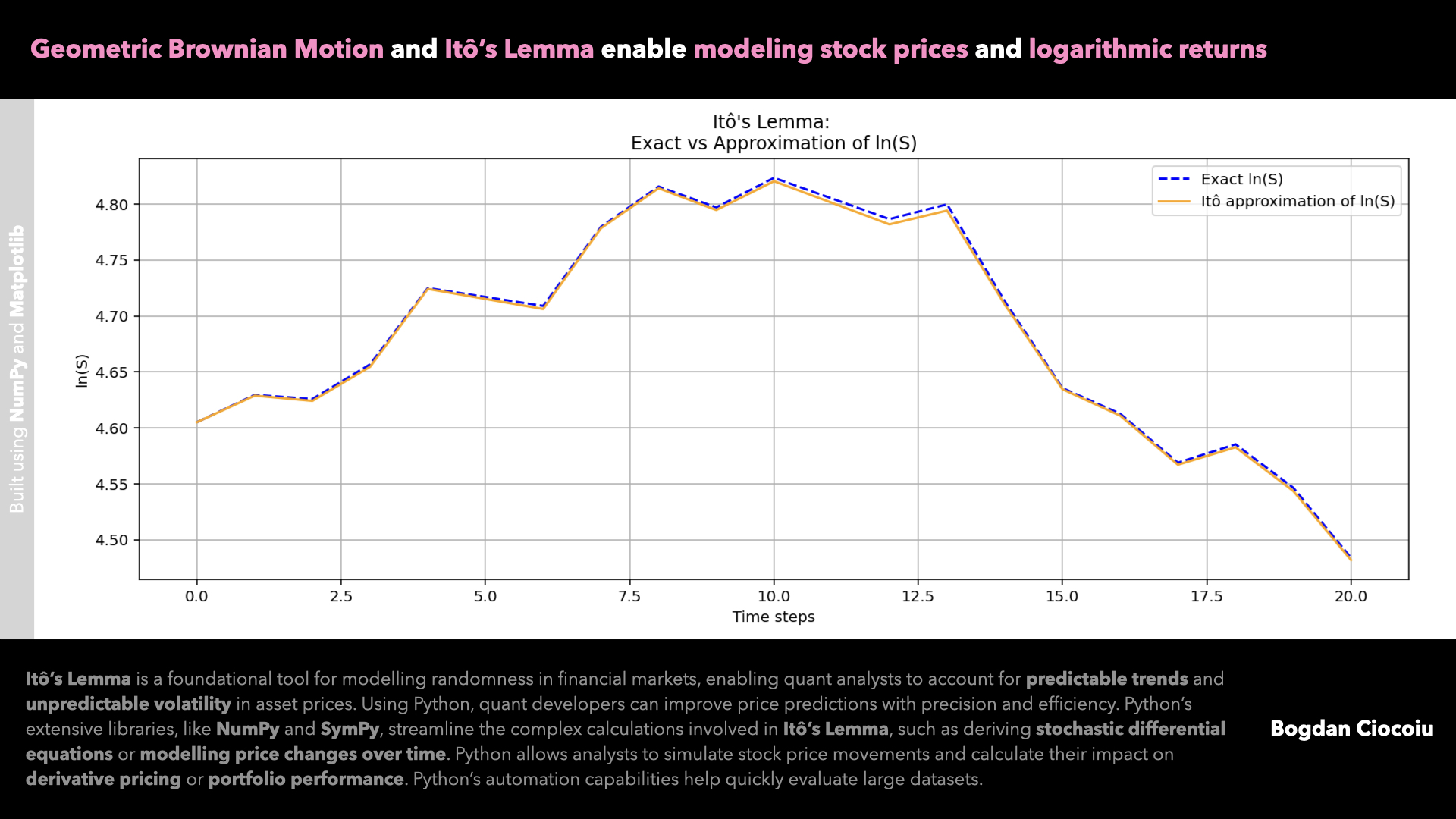

Price modelling – Itô’s Lemma – Geometric Brownian Motion

Quantitative analysts constantly seek robust methods to model and predict asset price movements. One such powerful tool is Itô’s Lemma, a cornerstone of stochastic calculus. By leveraging this mathematical framework alongside Python, quants can enhance their analytical toolkit, making strides in…

-

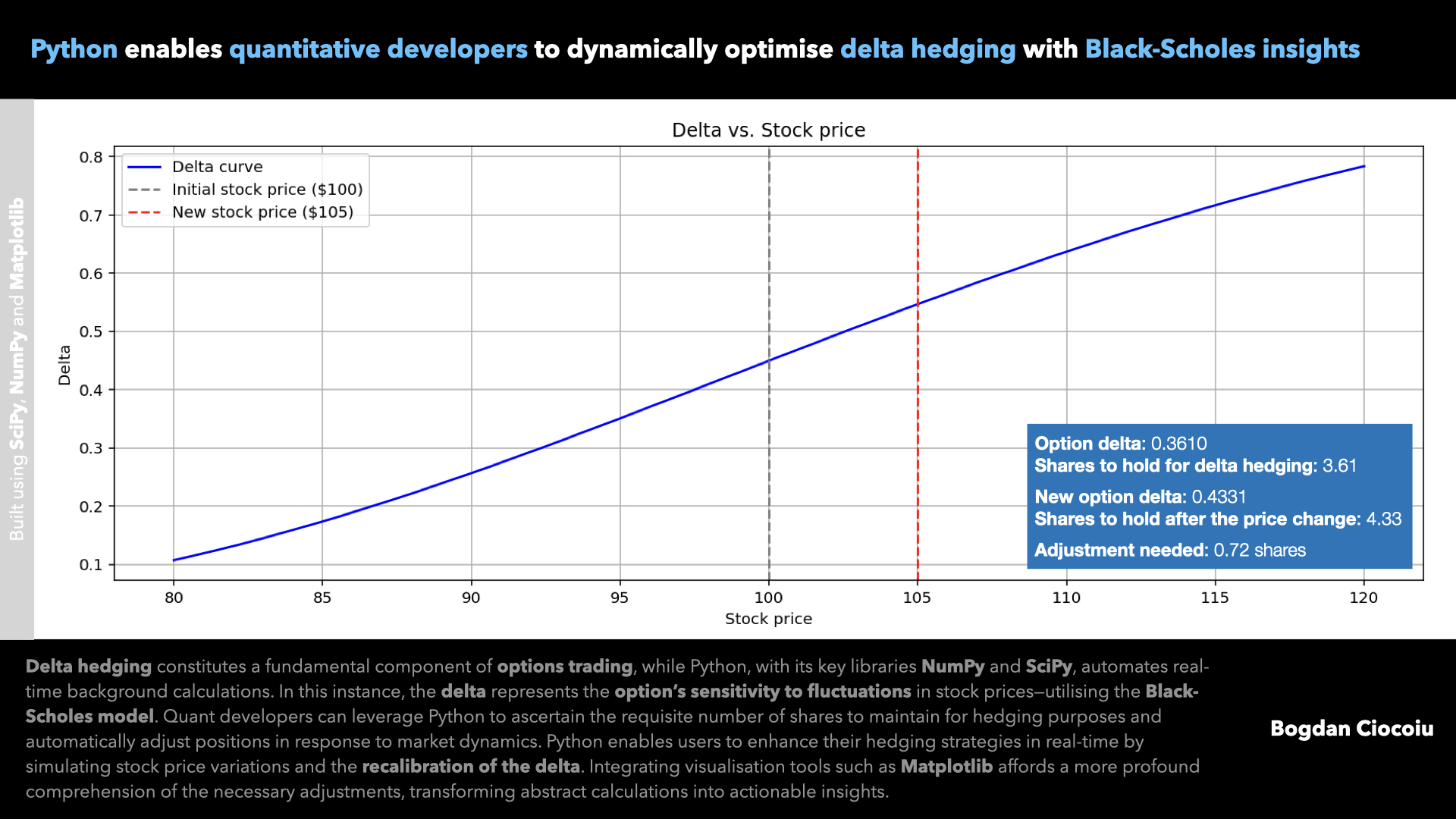

Delta hedging

Delta hedging is an essential technique in options trading, allowing traders to mitigate the risk of price fluctuations in the underlying asset. With Python, quant developers can access powerful tools for implementing and optimising this strategy, turning complex theoretical models…